featured

2026-07-10

Home

published

15- vs. 30-Year Mortgage: What You Need to Know Before You Choose

2017-04-24

- A 15-year mortgage can save you thousands in interest compared to a 30-year loan.

- 30-year mortgages offer lower monthly payments, making them easier to fit your budget.

- You’ll build home equity faster with a 15-year loan and own your home outright sooner.

- 15-year mortgages typically come with lower rates, reducing costs even more.

- A 30-year mortgage provides more flexibility to invest or handle unexpected expenses.

- You can combine both strategies by overpaying or refinancing a 30-year loan.

Buying a home is one of the biggest financial decisions most people will ever make, and the mortgage you choose plays a huge role in how that decision plays out over time. Two of the most common options are the 15-year and 30-year mortgages.

Understanding the key differences between a 15-year and a 30-year mortgage, besides term length, can save you a significant amount of money and stress in the long run.

How Each Loan Term Works

A mortgage is a loan you take out to purchase a home, and the term refers to how long you have to pay it back. With a 15-year mortgage, you agree to pay off the full loan balance within 15 years. With a 30-year mortgage, that repayment period is 30 years.

Both loan types typically come with a fixed interest rate, which means your rate stays the same the entire life of the loan. Your monthly payment has two main components:

- Principal: The portion of your payment that goes toward reducing your actual loan balance.

- Interest: The cost you pay to the lender for borrowing the money.

Early in any mortgage, most of your payment goes toward interest. Over time, more of your payment starts to go toward the principal. This process is called amortization, and it has a lot to do with why your chosen loan term has a huge effect on your total costs.

How Much More Will You Pay Monthly?

A 15-year mortgage will almost always have a higher monthly payment than a 30-year mortgage for the same loan amount. This is because you are paying off the same debt in half the time.

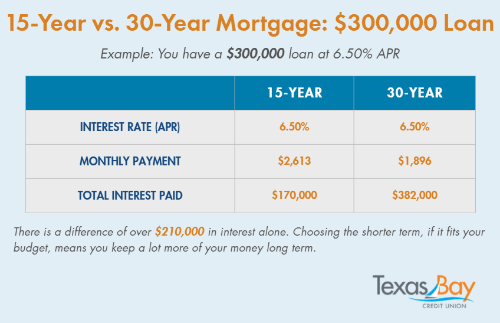

For example, on a $300,000 loan at a fixed interest rate of 6.50% APR, the approximate monthly payments would look like this:

- 15-year mortgage: Around $2,613 per month

- 30-year mortgage: Around $1,896 per month

That difference of more than $700 per month is significant for most households. That extra breathing room in the budget is why many buyers choose the longer term.

Total Interest Comparison: How Much More Does a 30-Year Mortgage Cost?

While the 30-year mortgage offers lower monthly payments, it comes with a much higher total cost over time. That is because you are paying interest for twice as long, and interest adds up fast.

Using the same example of a $300,000 loan at 6.50% APR:

- 15-year mortgage total interest: Approximately $170,000

- 30-year mortgage total interest: Approximately $382,000

That is a difference of over $210,000 in interest alone. Choosing the shorter term, if it fits your budget, means you keep a lot more of your money long term.

Why Shorter Terms Usually Have Lower Interest Rates

Another important distinction between the two loan types is the interest rate itself. Lenders typically offer lower interest rates on 15-year mortgages compared to 30-year mortgages because shorter loans pose less risk to the lender.

Even half a percentage point difference can add up to tens of thousands of dollars over the life of a loan. So, the 15-year mortgage features both a lower rate and a shorter repayment period, both of which will help you build equity and reduce overall costs.

When exploring your options, it is a good idea to ask your lender to show you side-by-side rate comparisons for both terms so you can see exactly what you would be paying in each scenario.

Which Mortgage Builds Equity Faster?

Equity is the portion of your home that you actually own. It is the difference between your home's market value and what you still owe on your mortgage.

Building equity quickly gives you access to tools like home equity loans or lines of credit, and it puts you in a stronger position if you decide to sell.

With a 15-year mortgage, you build equity much faster because more of each payment goes toward your actual loan balance from early on. With a 30-year mortgage, equity builds slowly at first because most of your payment goes toward interest.

This faster equity growth is one reason many financially stable homeowners prefer the 15-year term, especially if they plan to stay in their homes for many years.

30-Year Mortgage Benefits: Lower Payments and More Monthly Cash Flow

One of the strongest arguments for the 30-year mortgage is flexibility. When your monthly payment is lower, you have more money available each month to direct toward other financial goals. That could mean:

- Building up an emergency fund

- Contributing more to retirement accounts like a 401(k) or IRA

- Investing in the stock market or other assets

- Covering education expenses for children

- Handling unexpected costs without going into debt

This is one of the reasons why most homebuyers choose a 30-year mortgage.

Some financial advisors claim that if you invest the difference between a 15-year and 30-year payment and earn a solid rate of return, you might come out ahead despite paying more interest. This depends on market conditions and personal discipline, though.

The 30-year mortgage also provides a safety net. If your financial situation changes, such as a job loss or a major unexpected expense, a lower required payment gives you more room to adapt without risking your home.

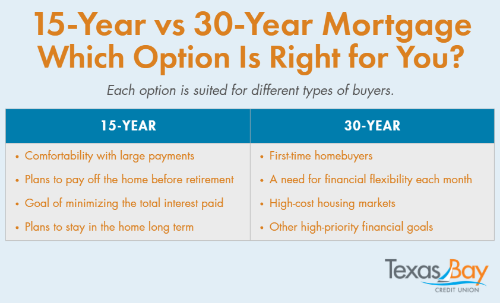

15-Year vs 30-Year Mortgage: Which Option Is Right for You?

There is no single right answer for everyone. The best mortgage term depends on your financial situation, goals, and comfort level with monthly obligations. With that said, there are some general patterns in who gravitates toward each option.

People who often prefer the 15-year mortgage include:

- Buyers with a stable, high income and comfortability with a larger payment

- Those who are focused on paying off their home before retirement

- Homeowners who want to minimize the total amount of interest they pay

- Buyers who will stay in the home long enough to benefit from fast equity growth

People who often prefer the 30-year mortgage include:

- First-time homebuyers who need to keep monthly costs manageable

- Those who want more financial flexibility each month

- Buyers in high-cost housing markets where a 15-year payment is too expensive

- Individuals who have other high-priority financial goals they are working toward

Can You Pay Off a 30-Year Mortgage Early?

Yes, and this is a strategy that many homeowners use to get the best of both worlds. If you take out a 30-year mortgage but make extra payments toward the principal, you can pay off your loan faster and reduce the total interest you pay.

This approach gives you the flexibility of a lower required payment while still allowing you to chip away at your balance more aggressively when your budget allows.

For example, one extra mortgage payment per year on a 30-year loan can shave several years off your repayment timeline. Even rounding up your monthly payment or adding a set amount each month to the principal can make a meaningful difference over time.

Before going this route, make sure your mortgage does not have prepayment penalties. Most conventional loans do not, but it is always worth confirming with your lender.

Switching from a 30-Year to a 15-Year Mortgage

Some homeowners start with a 30-year mortgage and later refinance into a 15-year loan once their financial situation improves or when interest rates drop. This can lock in a lower rate and accelerates payoff without making a higher payment from day one.

Refinancing comes with closing costs, so you should calculate how long it would take to break even on those costs with the savings gained from the new loan terms.

Use our Mortgage Refinance Calculator.

A mortgage specialist can help you run those numbers so you can decide if refinancing makes sense.

FAQ: 15-Year vs. 30-Year Mortgage Loans

Is a 15-year mortgage always better than a 30-year mortgage?

Not always. A 15-year mortgage saves significantly on interest and helps you pay off your home faster, but it comes with a higher monthly payment. A 30-year mortgage may be better if you need lower payments and more flexibility in your monthly budget.

What credit score do I need for a 15-year vs 30-year mortgage?

Both loan types typically require similar credit standards. Most lenders look for a minimum credit score of 620, but higher scores (700+) will help you qualify for better interest rates on either term.

Which mortgage is better if I plan to move in a few years?

If you don’t plan to stay long-term, a 30-year mortgage is often more practical because of its lower monthly payment and flexibility. The long-term interest savings of a 15-year loan matter less if you sell the home early.

What happens if I can’t afford my 15-year mortgage payment?

If your payment becomes unaffordable, you may need to refinance into a longer-term loan or explore hardship options. This is why it’s important to choose a loan that comfortably fits your budget.

Take the Next Step Toward Homeownership

Choosing between a 15-year and 30-year mortgage is not a decision to rush. Both options have advantages, and the right choice depends on your income, your financial goals, your lifestyle, and how much risk or obligation you are comfortable taking on.

The good news is that you do not have to figure it out alone. Texas Bay Credit Union offers personalized mortgage guidance to help you compare your options, understand the numbers, and find a loan that truly fits your life.

Reach out today to speak with a mortgage specialist and take the next step toward owning a home with confidence.