featured

2026-06-30

Insurance

published

What Houston Homebuyers Need to Know About Flood Insurance

2017-04-24

- Houston area homebuyers face high flood risk due to terrain, rainfall, and coastal storms

- Flood insurance is not included in standard homeowners insurance policies

- Flood zones in Greater Houston determine risk level, insurance requirements, and premiums

- Flood insurance costs vary based on elevation, location, and property value

- NFIP and private flood insurance offer different coverage options for homes in Houston

- Checking flood zone, flood history, and insurance quotes protects Houston area homebuyers

If you are buying a home in Greater Houston, there is one topic you need to carefully consider before you sign anything: flood insurance.

Living in a region that sits along the Gulf Coast, crosses multiple bayous, and receives some of the heaviest rainfall in the United States comes with serious flood risk. That is why researching flood insurance options will help you protect your finances as a homeowner.

Why Flood Risk Is Such a Big Deal in Houston

The Houston area has experienced several catastrophic flooding events in recent decades, and it’s not by chance.

Reasons flood risk is higher in Greater Houston include:

- Low elevation and flat terrain mean water has nowhere to go quickly.

- Bayous and waterways run through neighborhoods and can overflow during storms.

- Urban development has replaced natural green space with concrete and pavement, reducing the land’s ability to absorb rainfall.

- Proximity to the Gulf Coast means tropical storms and hurricanes are a real seasonal concern.

None of this means you should avoid buying a home in Houston. It just means you need to go in with your eyes open.

Does Standard Homeowners Insurance Cover Flooding?

Standard homeowners insurance does not cover flood damage. If a pipe bursts inside your home, you are typically covered. But if a severe storm causes water to enter your home from outside, that is a flood event, and a standard policy will not pay for it.

Flood insurance is a completely separate policy, and you need to purchase it in addition to your homeowners coverage. There are two main sources for flood insurance:

- The National Flood Insurance Program (NFIP) is managed by FEMA and available through many insurance agents. NFIP policies cover up to:

- $250,000 for your home's structure

- $100,000 for personal contents

- Private flood insurance is available through independent insurers. These policies sometimes have higher coverage limits and additional options not offered by the NFIP.

Your lender will tell you whether flood insurance is required, but even if it is not, it is worth considering carefully.

What Is a Flood Zone and How Do You Find Yours?

FEMA divides land into flood zones based on risk level. When you are buying a home in the Houston area, knowing the property's flood zone designation is essential.

Here is a quick breakdown of the most common designations:

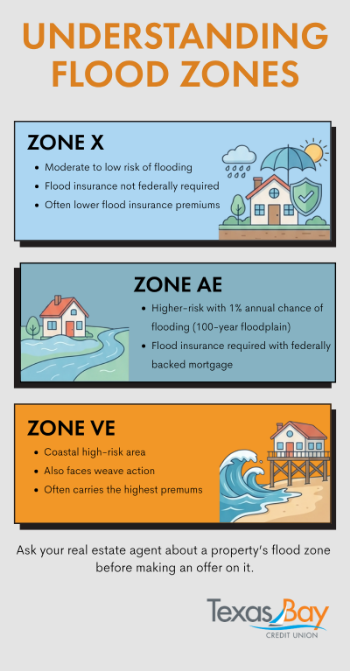

- Zone X is considered a moderate to low-risk area. Flood insurance is not federally required here, but it is still a wise idea given Houston's weather history.

- Zone AE is a high-risk area with a one percent annual chance of flooding (sometimes called the 100-year floodplain). Flood insurance is required if you have a federally backed mortgage.

- Zone VE is a coastal high-risk area that also faces wave action. These properties carry the highest premiums.

Ask your real estate agent about a property’s flood zone before making an offer on it.

Keep in mind that flood maps are updated periodically, and a home currently in a low-risk zone may be remapped into a higher-risk zone after you purchase it. This is another reason to think ahead.

How Much Does Flood Insurance Cost?

Flood insurance costs vary based on several factors, including:

- Flood zone

- Age and elevation of the home

- Amount of coverage you choose

Under FEMA’s current risk rating system, called Risk Rating 2.0, two homes on the same street can have very different premiums due to an individualized assessment of each property's risk.

Here are some general factors that influence your premium:

- The elevation of your home relative to the Base Flood Elevation in your area

- The distance of the property from water sources like bayous or reservoirs

- The cost to rebuild the structure

- Whether you choose NFIP coverage or a private policy

As a rough reference point, the average NFIP policy in Texas costs somewhere in the range of $700 to $1,000 per year, but many Houston properties fall above that range depending on risk. Getting a quote early in the homebuying process will help you budget accurately.

What Flood Insurance Does and Does Not Cover

Even once you have a policy, it is important to understand exactly what is and is not included. Flood insurance covers direct physical damage caused by flooding, but there are limits and exclusions you should know about.

Typical flood insurance will cover:

- The structure of your home, including the foundation, walls, electrical and plumbing systems, HVAC equipment, and built in appliances

- Personal belongings such as furniture, clothing, and electronics (if you have contents coverage)

Flood insurance generally does not cover:

- Temporary housing or living expenses while your home is being repaired

- Vehicles (your auto insurance may cover flood damage to your car under comprehensive coverage)

- Landscaping, decks, fences, or detached structures like sheds unless specifically included

- Damage caused by moisture or mold that was not directly related to the flood event

Reading the fine print and asking your insurance agent specific questions about what your policy includes is always worth the extra time.

Practical Steps Before You Buy

There are several smart moves you can make during the homebuying process to protect yourself when it comes to flood risk.

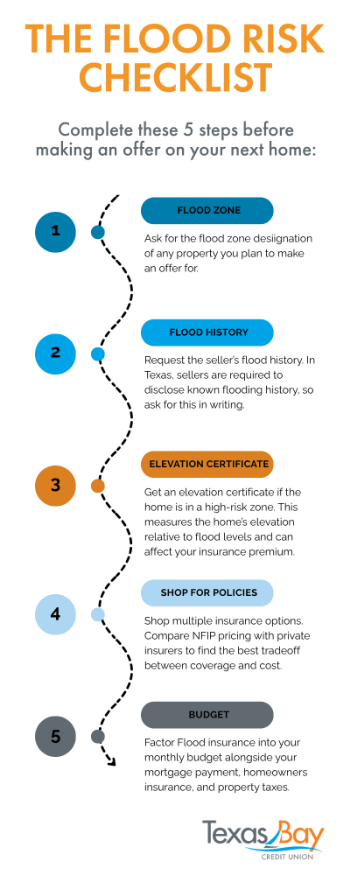

- Ask for the flood zone designation of any property you are seriously considering before making an offer.

- Request the seller's flood history. In Texas, sellers are required to disclose known flooding history, so ask for this information in writing.

- Get an elevation certificate if the home is in a high-risk zone. This document measures the home's elevation relative to flood levels and can directly affect your insurance premium.

- Shop multiple insurance options. Compare NFIP pricing with private insurers to find the best combination of coverage and cost.

- Factor flood insurance into your monthly budget alongside your mortgage payment, homeowners insurance, and property taxes.

.png)

FAQ: Flood Insurance in Greater Houston

Is flood insurance required when buying a home in Houston?

Flood insurance is required for Houston area homes in high-risk flood zones (like AE or VE) if you have a federally backed mortgage, but it is optional in lower-risk areas.

What flood zone is my property and why does it matter?

A property’s flood zone, assigned by FEMA, determines its flood risk level, whether insurance is required, and how much you will pay in premiums. You can look up your property on FEMA’s website: FEMA Flood Map Service Center | Search By Address.

Is there a waiting period for flood insurance in Houston?

Most flood insurance policies, especially through NFIP, have a 30-day waiting period before coverage begins, so buyers should secure a policy well before closing.

When should I buy flood insurance during the homebuying process?

Houston area homebuyers should start shopping for flood insurance during the option period or early in underwriting to avoid delays and ensure coverage is active by closing.

Can a seller transfer their flood insurance policy to the new buyer?

Yes, in many cases a seller’s flood insurance policy can be transferred to the buyer, potentially helping avoid waiting periods and preserving favorable rates.

Does flood insurance cover newly built homes in Houston

Yes, new construction homes in can be covered, but premiums will depend on elevation, location, and compliance with current floodplain regulations.

Make a Confident Move Into Homeownership

Buying a home in Houston is a powerful investment, and arriving prepared makes all the difference. At Texas Bay Credit Union, we help you master every step of the homebuying journey, from securing the right mortgage to setting up your long-term financial success.

Before closing day, remember to research local flood zones, secure your insurance quotes early, and ask plenty of questions. The more informed you are today, the more confident you will feel the moment you hold those keys.

Protect what matters most. Reach out to our insurance specialists today to safeguard your new home and family.