featured

2026-03-18

Home

published

Mortgage Recast vs. Refinance: How to Lower Your Home Payment in Houston

2017-04-24

- A mortgage recast is a lump-sum payment that lowers your monthly bill payment while keeping your current interest rate and term.

- A mortgage refinance is a new loan that replaces your old one to help you secure a lower interest rate, if available, or change your loan term.

- Recasting is generally for conventional loans only, while refinancing and recasting are both available for FHA, VA, and USDA loans.

- Recasts cost a flat fee, while refinances can cost 2%–6% of the loan balance in closing costs.

- A recast requires no credit check or appraisal, while a refinance requires a full credit "hard pull" and a new home valuation.

If you’re a homeowner in the Greater Houston area, you’re likely seeking ways to lower your monthly mortgage payment as your property taxes and/or insurance rates continue to increase.

Depending on your finances and how the current real estate market in Houston can affect you, there are two ways you can adjust your monthly mortgage payment:

- Mortgage Recast

- Mortgage Refinance

Determine which one is best suited to help you save each month.

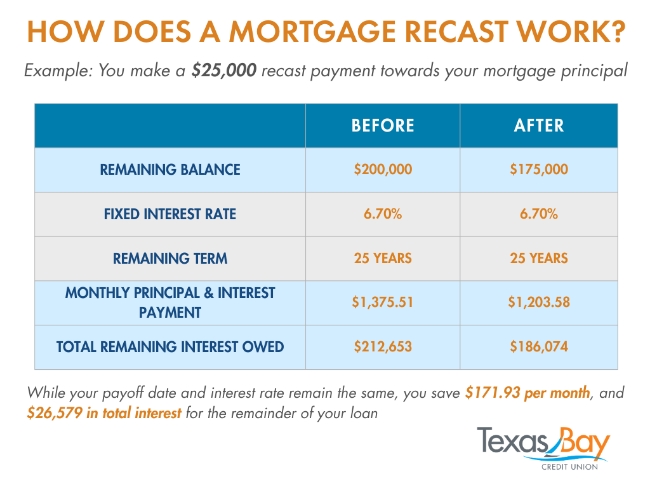

What Is a Mortgage Recast?

A mortgage recast is a one-time lump-sum payment you can make towards your mortgage principal. Your balance is lower, but your term and interest rate stay the same, resulting in a lower monthly mortgage payment.

Is a Mortgage Recast Right for Me?

There are three things to consider before recasting your mortgage:

- Your interest rate stays the same. If you bought your home before rates surged in Houston in 2022, you likely want to keep your low rate. While refinancing your home will likely change your interest rate, a recast ensures it stays the same.

- A recast requires upfront costs. Lenders often require a minimum recast payment and a processing fee. Ask your lender about these. If you have cash available from savings or a bonus, a recast could be a great way to reduce monthly payments.

- Your term stays the same. While some homeowners use a refinance to either shorten their term and pay off their debt faster, or lower their monthly payment with a longer term, a recast ensures your term doesn’t change.

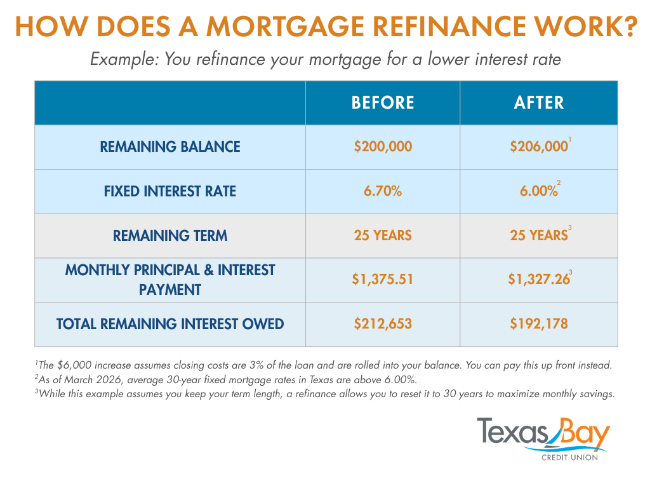

What Is a Mortgage Refinance?

A mortgage refinance is the process of replacing your home loan with a new one, rather than adjusting your existing one like a recast. While the principal stays the same, you potentially change your:

- Interest Rate

- Remaining Term

- Lender

A lot more variables are in play with a refinance than with a recast, so carefully research whether it’s right for you.

Should I Refinance My Mortgage?

Four things can help you determine if refinancing your mortgage is right for you:

- Your interest rate will change. If your interest rate is lower than the current rates in Houston, it will likely rise if you refinance. Only consider refinancing if you’re paying a higher-than-average rate.

- Refinancing involves closing costs. Most lenders will require that you pay for an appraisal, loan origination fees, and other costs that can add up to between 2% and 6% of your loan. Ask your lender about these fees and calculate how long it would take for your new monthly savings to offset them. If you plan to move soon, refinancing may not be right for you.

- You can change your term length. Because you’re opening a new loan, refinancing allows you to shorten your term to become debt-free sooner or lengthen it for a lower monthly payment.

- You can change your lender. If you’re considering refinancing your loan because you’re unhappy with your current lender’s terms, you have the freedom to find another. Reach out to Texas Bay’s mortgage team to learn if refinancing with a TBCU home loan is right for you.

FAQ: Mortgage Recast vs. Refinance in Houston

Can I recast my mortgage more than once?

Yes. Unlike a refinance, which involves a brand-new contract and closing costs, most lenders allow you to recast multiple times over the life of your loan. If you receive a bonus this year and an inheritance next year, you can perform a recast each time to keep your monthly payment down. Just be aware that you will likely pay the flat administrative fee for each request.

Does a mortgage recast affect my credit score?

No. Because a recast is an adjustment to your existing loan, there is no "hard pull" on your credit report. This makes it an ideal option for homeowners who are planning other large purchases, like a car, who don't want a temporary dip in their credit score that often comes with a refinance application.

Can I recast a mortgage I just signed last month?

Usually not, because most lenders require a waiting period of on-time payments before approving a recast. For Texas Bay, that period is 120 days.

How much lower should my interest rate be to justify a refinance?

It depends on your break-even point. If your closing costs are $6,000 paid up front and you save $150 a month, you must stay in your home for at least 40 months to make the change profitable.

Are there any costs involved in refinancing my mortgage?

Yes, refinancing typically includes closing costs, including application fees, origination fees, appraisal fees, and title search and insurance fees. Ask your lender for these costs before refinancing.

What credit score do I need to refinance my home loan?

The minimum credit score required to refinance depends on your lender. In the case of Texas Bay Credit Union, you would need a credit score of at least 620 to qualify for a mortgage refinance.

Choosing Your Path to a Lower Payment With Texas Bay

Whether you choose a mortgage recast or a mortgage refinance, don’t guess when it comes to taking the edge off your monthly mortgage payment. The mortgage experts at Texas Bay are here to help you choose the solution that suits your needs.

Ready to see how much you can save? Ask our team how we can help you make homeownership in Houston more affordable.