not featured

2026-04-30

Vehicle

published

What Is GAP, and Do You Need It?

2017-04-24

- GAP protection covers the difference between your loan balance and your car’s value if it's stolen or totaled.

- Most new cars depreciate by 20% in the first year, often leaving you owing more than the vehicle is worth.

- If a total loss occurs, GAP waives the remaining debt that your primary insurance settlement doesn't cover.

- GAP Protection prevents you from paying out of pocket for a vehicle you can no longer drive.

- Texas Bay Credit Union offers GAP Protection with auto loans, giving drivers added peace of mind when financing their next vehicle.

Buying a vehicle involves financial decisions that can affect your budget for years. A common question borrowers ask when financing is whether GAP Protection is worth it. For many drivers, especially those financing newer vehicles or making smaller down payments, the answer largely depends on how much they owe on their car loan compared to the car’s market value.

What Is GAP?

GAP stands for Guaranteed Asset Protection. It’s specifically designed to bridge the "gap" between your primary auto insurance settlement and the remaining balance on your loan if your vehicle is stolen or declared a total loss.

As the Consumer Financial Protection Bureau notes, standard auto insurance typically only pays out the current market value of the car, which may not cover what you still owe.

Drivers who are most at risk of this financial gap are:

- Making a down payment of less than 20%

- Financing a vehicle for 60 months or longer

- Rolling negative equity from a previous vehicle into a new loan

In these cases, your loan balance can remain higher than the vehicle’s actual value for a long period, especially during the early years of ownership.

How Does GAP Work?

The Texas Department of Insurance notes that a new car loses value quickly and is considered used the moment it leaves the lot. According to Kelley Blue Book, you might see a depreciation of 20% in the first year.

If a total loss occurs during this time, your insurance company will pay a settlement based on that depreciated value, which may not be enough to cover what you still owe on your loan.

However, if you had added GAP to your auto loan, you could get your remaining balance waived by your lender, effectively clearing the debt that your insurance didn't cover.

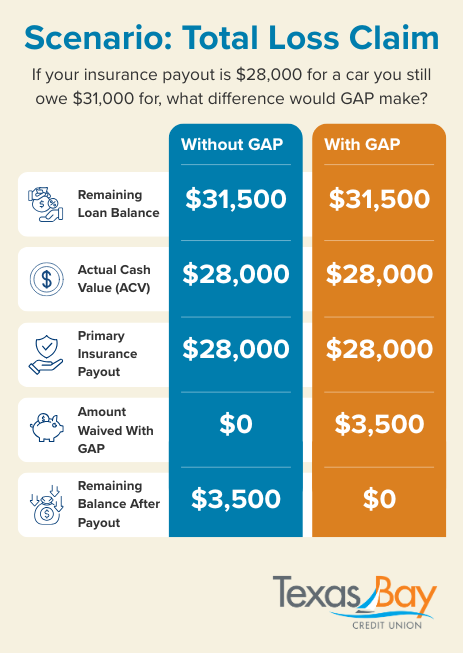

Here is a simple example. Imagine you finance a car for $35,000. A year later, after depreciation, the vehicle’s actual cash value is $28,000, but your loan payoff is still $31,500. If the car is totaled, your insurer may pay close to the actual cash value rather than the full payoff amount. Without GAP Protection, you could still owe the remaining difference out of pocket. That remaining amount is exactly the risk that GAP is intended to address.

This is even more important for borrowers who choose longer loan terms for lower monthly payments. The CFPB notes that longer auto loans can leave borrowers in negative equity for a longer period, meaning they owe more than the vehicle is worth. That doesn’t mean everyone with a long-term loan needs GAP, but it does mean the risk stays with them longer.

What GAP Typically Covers

GAP Protection addresses a financial shortfall after a covered total loss. If your vehicle is stolen or totaled and your insurance company pays less than your remaining loan balance, GAP can help cover that difference, subject to the terms of the contract or policy. That is why borrowers see GAP as an additional layer of protection.

GAP is not the same as collision or comprehensive coverage. Your primary auto policy still plays the primary role in a claim. GAP only becomes relevant after the primary insurer determines the vehicle’s value and issues the settlement. In other words, it fills in the space (or gap) that can remain after the standard claim is settled.

What GAP May Not Cover

The Texas Department of Insurance (TDI) warns that many GAP products have exclusions for what they cover on a claim. Examples listed by TDI include:

- Overdue payments

- Unpaid finance charges

- Warranty costs

- Balloon payments

- Deductibles

- Damage from a prior accident

So, read the fine print. Two GAP products that appear similar could have crucial differences in how they cover your loss. Before you agree to any coverage, review the contract and ask:

- What is excluded?

- How are claims handled?

- Are there conditions that could reduce the benefit?

The CFPB also advises consumers to compare prices and coverage before buying because costs can vary significantly.

When GAP May Make Sense

Loans with a small down payment

TDI points to down payments below 20 percent as the point where the gap between the value and the loan balance can reach thousands of dollars. Starting with less equity often means less cushion if the vehicle is totaled early in the loan.

Longer loan terms

TDI highlights financing terms of 60 months or more, and the CFPB notes that longer terms can keep borrowers in negative equity longer. This does not mean long-term financing is always a mistake. It simply means the financial math can create a period when you owe more than the car is worth, which is exactly the risk GAP is built to address.

Financing a new car

New cars depreciate rapidly in the first year of ownership, widening the gap between market value and the loan balance. However, used vehicles can also raise the question of GAP, depending on the price, loan structure, and the equity you have at the start.

Peace of mind

Borrowers who want predictable financial protection often appreciate GAP because it can reduce the risk of having to make payments on a vehicle they no longer own. That is especially relevant for households that rely on a vehicle every day for commuting, family responsibilities, or work. A total loss is stressful enough without the added pressure of an unpaid loan balance.

Where Can You Buy GAP Coverage?

You can often find GAP Protection plans offered with your loan by your auto lender, like your dealership, bank, or credit union. When comparing lenders, carefully review both their loan terms and GAP Protection plans.

Frequently Asked Questions About GAP Protection

What is the difference between GAP insurance and a GAP waiver?

While both cover the same financial "gap," GAP insurance is a standalone policy sold by insurance companies. A GAP waiver is a debt cancellation agreement offered directly by your lender, like Texas Bay, that waives your remaining loan balance if the car is totaled.

Can I cancel GAP protection if I no longer need it?

Yes. If you pay off your loan early, sell the vehicle, or reach a point where you owe less than the car is worth, you can typically cancel your GAP coverage.

Does GAP cover car theft?

Yes, GAP Protection can be used in the event of an unrecoverable theft. Once your primary insurance issues a settlement for the vehicle's market value, GAP is used to address the remaining balance on your loan.

Does GAP protection cover a blown engine or mechanical repairs?

No. GAP protection only applies when a vehicle is declared a total loss. It does not cover mechanical breakdowns, routine maintenance, or wear and tear. For those issues, you would need Mechanical Breakdown Protection.

Should I get GAP protection for a used car?

While most commonly associated with new cars, GAP can be valuable for used cars if you have a high-interest rate, long loan term, or low down payment.

Protect Your Auto Loan With GAP Protection From Texas Bay

Instead of facing the difference between your insurance settlement and your remaining loan balance on your own, you can choose coverage that helps close that gap and gives you greater peace of mind.

Texas Bay Credit Union offers GAP Protection with our auto loans to help borrowers safeguard their finances and stay better prepared for the unexpected. Whether you’re purchasing a new vehicle or financing a used one, adding GAP Protection can help you feel more confident that your loan is protected if your car is stolen or declared a total loss.

Don't let negative equity stall your financial future. Speak with a Texas Bay expert about how to protect your next auto loan with GAP.