not featured

2026-06-16

Vehicle

published

When to Refinance Your Auto Loan

2017-04-24

- Lower Your Rate: Refinancing replaces your current auto loan with a new one at a lower interest rate.

- Big Savings: Lowering your rate can save you hundreds of dollars in total interest.

- Know When to Act: Refinance if your credit improved, rates dropped, or you used dealership financing.

- Credit Union Advantage: Member-owned credit unions offer lower interest rates and fees than traditional banks.

-

Easy Process: Prequalify, pick your term, and let the new lender pay off your old loan.

The rate and terms on your auto loan could no longer be the best deal available to you. And with average monthly payments for new vehicles now exceeding $770, according to data from Edmunds, any opportunity to lower these costs is worth exploring.

Knowing when to refinance your auto loan could save you a meaningful amount of money, lower your monthly payment, or both. The key is knowing when the timing is right.

What is Auto Loan Refinancing and How Does It Work?

Auto loan refinancing is the process of replacing your current car loan with a new loan, ideally featuring a lower interest rate, better terms, or a lower monthly payment. This does not change the car you drive, but it can make a big difference in how much you pay throughout the loan.

When you apply for a refinance, your new lender pays off your original loan balance in full. You then begin making monthly payments to the new lender under your newly approved interest rate and loan term structure.

When is the Best Time to Refinance Your Car Loan?

There are several situations where refinancing your auto loan may make sense:

1. Your credit score has improved.

Your credit score at the time you financed your car played a major role in the interest rate you received. If you have paid bills on time, reduced debt, or given your credit history time to mature since then, your score may now qualify for a lower rate.

2. Interest rates have dropped.

Rates today may look very different from when you took out your original loan. Even a small reduction in your interest rate can save you hundreds of dollars over the remaining life of the loan.

3. You used dealership financing.

Dealer financing is convenient, but not always the best option. Dealers sometimes mark up interest rates as part of their profit model. Refinancing through a credit union can help you find better rates.

4. Your monthly payment feels unmanageable.

If your budget has tightened and your car payment is putting strain on your finances, refinancing to extend the loan term can reduce your monthly obligation. Just be aware that extending the term may mean you pay more in total interest over time. Some credit unions, like Texas Bay, also offer 90 days of no payments and skip-a-payment opportunities for qualifying loans.

5. You want to pay off the loan faster.

If your income has increased and you want to get out of debt sooner, refinancing into a shorter term at a lower rate could help you do that without dramatically increasing your monthly payment.

6. You financed a used vehicle at a high rate.

Data from Experian shows that the average used car payment has reached $537 per month. If you bought a used vehicle at a higher rate, refinancing could bring your payment down considerably.

When Should You Avoid Refinancing an Auto Loan?

Refinancing your auto loan may not work in your favor if:

1. Your loan is nearly paid off.

If you only have a year or less left on your loan, the savings from a lower interest rate may not outweigh the fees involved in refinancing. Run the numbers carefully before moving forward.

If you only have a year or less left on your loan, the savings from a lower interest rate may not outweigh the fees involved in refinancing. Run the numbers carefully before moving forward.

2. Your vehicle has high mileage or is significantly depreciated.

Lenders consider the vehicle's value when approving a refinance. If your car is worth considerably less than what you owe, or has accumulated many miles, some lenders may not approve the refinance or may offer less favorable terms.

Lenders consider the vehicle's value when approving a refinance. If your car is worth considerably less than what you owe, or has accumulated many miles, some lenders may not approve the refinance or may offer less favorable terms.

3. Your current loan has prepayment penalties.

Some loans include fees for paying off the balance early. Check your current loan agreement to ensure refinancing will not trigger a penalty that would eat into your savings.

Some loans include fees for paying off the balance early. Check your current loan agreement to ensure refinancing will not trigger a penalty that would eat into your savings.

4. Your credit has declined.

If your credit score has dropped, refinancing could result in a higher interest rate than what you currently have. In that case, focus on rebuilding your credit before applying.

If your credit score has dropped, refinancing could result in a higher interest rate than what you currently have. In that case, focus on rebuilding your credit before applying.

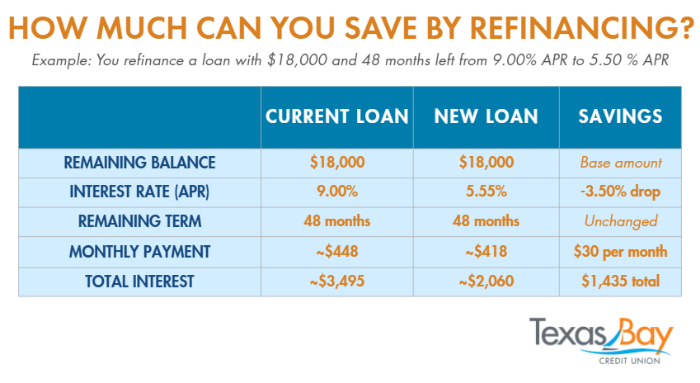

How Much Money Can You Save by Refinancing?

The savings from refinancing depend on several factors, including:

- Your remaining loan balance

- The difference in interest rates

- Number of months left on your loan

Consider this example.

Suppose you have a remaining balance of $18,000 on a loan with a 9.00% Annual Percentage Rate (APR) and 48 months left to pay. If you refinance to a 5.50% APR with the same term, you could save over $1,400 in interest over the life of the loan and reduce your monthly payment by roughly $30 each month. The more you owe and the greater the rate difference, the larger your potential savings.

Use our auto loan refinance calculator to understand your situation before you apply.

How to Choose the Best Auto Refinance Lender

Your lender matters as much as your rate. Look for the following when comparing options:

1. Competitive interest rates.

Credit unions tend to offer lower rates than traditional banks because they are member-owned and not profit-driven.

2. Reasonable fees.

Make sure any fees associated with the new loan do not cancel out your interest savings. Ask potential lenders about their processing, origination, and early repayment fees. For example, Texas Bay features a $0 refinance fee policy with no hidden application costs.

3. Flexible loan terms.

A good lender will give you options, whether you want to pay off the loan faster or extend your term to lower your monthly payment.

A good lender will give you options, whether you want to pay off the loan faster or extend your term to lower your monthly payment.

4. Easy application process.

Look for a lender with a straightforward application, clear communication, and helpful staff to walk you through the process.

5. Strong member or customer service reputation.

Read reviews and ask around. A lender that treats you well and answers your questions honestly is worth its weight in savings.

How to Refinance a Car Loan: A Step-by-Step Guide

1. Check your current loan details.

Pull out your loan agreement and note your interest rate, remaining balance, monthly payment, and whether there are any prepayment penalties.

Pull out your loan agreement and note your interest rate, remaining balance, monthly payment, and whether there are any prepayment penalties.

2. Review your credit report.

Before applying anywhere, check your credit report for errors and get a sense of where your score stands. You are entitled to a free report from each of the three major bureaus once per year at AnnualCreditReport.com.

Before applying anywhere, check your credit report for errors and get a sense of where your score stands. You are entitled to a free report from each of the three major bureaus once per year at AnnualCreditReport.com.

3. Shop around for rates.

Get quotes from at least two or three lenders. Use Texas Bay’s online calculator to compare different terms, rates, and payoff plans.

Get quotes from at least two or three lenders. Use Texas Bay’s online calculator to compare different terms, rates, and payoff plans.

4. Gather your documents.

Most preliminary auto loan refinance applications request your vehicle and loan details, proof of income, driver’s license, and proof of insurance.

Most preliminary auto loan refinance applications request your vehicle and loan details, proof of income, driver’s license, and proof of insurance.

5. Submit your application.

Once you have chosen a lender, complete the full application. If approved, the new lender will pay off your old loan directly and set up your new loan terms.

Once you have chosen a lender, complete the full application. If approved, the new lender will pay off your old loan directly and set up your new loan terms.

6. Continue making payments.

Until your old loan is officially paid off and the new loan is set up, keep making your regular payments to avoid any late fees or marks on your credit.

Until your old loan is officially paid off and the new loan is set up, keep making your regular payments to avoid any late fees or marks on your credit.

The Benefits of Refinancing Your Auto Loan with a Credit Union

Credit unions are member-owned financial cooperatives. They return profits to members through lower loan rates, higher savings rates, and reduced fees.

Benefits of refinancing with a credit union include:

- Lower Rates: Competitive pricing usually beats traditional banks.

- Fewer Fees: Profit-sharing model reduces extra costs.

- Member Focus: Decisions prioritize your financial well-being.

FAQ: Refinancing Your Auto Loan

Can you refinance a car loan with bad credit?

Yes, you can refinance with bad credit, but it is much more difficult to secure a lower interest rate. If your credit score has dropped since you bought the car, refinancing may actually increase your rate. Your best strategy is to apply with a co-signer who has strong credit, or focus on rebuilding your score before applying.

Does refinancing a car loan hurt your credit score?

Refinancing will cause a temporary, minor drop in your credit score. This happens because lenders use a hard credit pull to review your application. However, your credit will recover as long as you continue making payments on time.

Do I need a down payment to refinance a car?

No, a down payment is typically not required for most auto refinancing applications. The new loan simply covers the exact remaining payoff balance of your original loan. Drivers with negative equity in their vehicles may be an exception to this, but this would also depend on other factors like creditworthiness.

Can you refinance an auto loan immediately after buying a car?

Yes, you can legally refinance the day after you sign your original loan, as there are no waiting period laws. However, it is smartest to wait 60 to 90 days. This ensures your new lender can cleanly transfer the lien.

What documents do I need to prepare for auto refinancing?

You will typically need these items to refinance your auto loan:

- 15 day payoff letter at the time of closing

- Proof of income

- 2 most current paystubs for W2 employees

- 2 most current years of tax returns for self-employed drivers

- Declaration page with the lienholder added

- Insurance card

- Drivers license

Other items may apply depending on the driver’s scenario.

Take Control of Your Loan Today

Whether you want a lower payment, a faster payoff, or simply a better rate, now is a great time to review your current loan and see what is possible. Reach out to Texas Bay Credit Union to explore your refinancing options and find out how much you could save.