featured

2026-01-16

Home

published

How to Apply for a Home Equity Loan or HELOC in Houston: A Step-by-Step Guide

2017-04-24

- Under Texas law, total home debt (mortgage + new loan) cannot exceed 80% of a home's fair market value.

- Use the county appraisal district website to find your home’s estimated value.

- Check your most recent mortgage statement to verify your remaining balance.

- Locate official income documentation like pay stubs or tax returns to show you can make loan payments.

The equity in your home can be the key to checking off a major goal, whether it’s consolidating high-interest debt or starting a home renovation.

We know the loan application process can be slow and daunting, so our home equity loan application guide will help you avoid common mistakes for a smoother approval.

Start with our Home Equity Loan & Home Equity Line of Credit (HELOC) Application Worksheet:

Use the details below to work through the phases outlined in the worksheet.

Phase 1: Conditional Pre-Approval

Phase 1 on our worksheet will guide you through our online application and obtain Conditional Pre-Approval. You should be ready to answer the following questions:

Does your mortgage payment include taxes and insurance, or do you pay them separately?

Check your mortgage statement:

-

- If “Escrow” is listed, your payment includes taxes and insurance.

- If “Escrow” isn’t listed, you likely pay taxes and insurance separately.

Which product are you applying for?

Our blog covers the difference between a home equity loan and a HELOC. Whether it’s your first or second lien depends on your mortgage.

Choose “1st Lien” if either of the following is true:

-

- Your mortgage is paid off

- You plan to refinance your existing mortgage

If you don’t plan to refinance your existing mortgage loan, choose the “2nd Lien” option.

What is your gross annual income (before taxes)?

Your answer must match your paystubs or tax returns, which you’ll need to submit later. Inconsistent income information is the most common reason for delays or denials.

If you’re employed:

-

- Use your two most recent pay stubs.

- Submit your gross amount before taxes.

If you’re self-employed:

-

- Use your two most recent tax returns.

- Submit your income after business expenses—your Net Profit.

- Make sure the amount is before taxes.

What is your estimated property value?

Submit the most current value you can find. It will be used to determine how much you can borrow. Your local government’s appraisal district website, like Harris Central Appraisal District (HCAD), is a trusted and free resource to find this.

What is your current mortgage balance?

Get this answer from your most current mortgage statement. This will also be used to determine how much you can borrow.

What loan amount and term are you requesting?

Calculate the maximum amount you can borrow before answering.

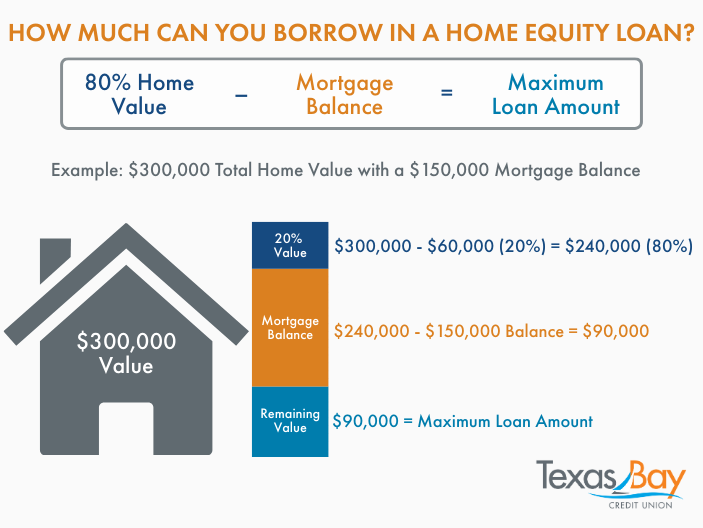

Remember the 80% rule: 80% Home Value – Mortgage Balance = Your Maximum Loan Amount

Example: If HCAD says your home is worth $300,000, 80% of that is $240,000. If you owe $150,000 on your mortgage, you could potentially borrow up to $90,000.

Answering with a higher amount will risk your application getting denied.

Ensuring the information above is accurate and complete puts you on the right track while your application is reviewed for Conditional Pre-Approval. Once completed, you’ll be halfway there.

Phase 2: Full Pre-Approval

You need three documents to qualify for full pre-approval:

- Proof of Income

- Homeowner’s Insurance Declaration Page

- Current Mortgage Statement (If Applicable)

Follow the Phase 2 checklist in your worksheet to make sure your application is complete:

Proof of Income

Get the most recent versions of these documents.

-

- Primary Income: Choose option A, B, or C, depending on which applies to you. Get pay stubs from your employer, tax returns from your IRS account, or retirement or disability award letters from your “my Social Security” account.

- Secondary Income: Check options D through H and gather any income documentation that applies to you.

Checkmark each document on your worksheet as well as Proof of Income.

Your Homeowner’s Insurance Declaration Page

You’ll specifically need the Declaration Page. Search this document for each of the four items under this section in your worksheet. Checkmark each one on the worksheet as you find it, and then checkmark Homeowner’s Insurance Declaration Page once you’ve finished.

Your Current Mortgage Statement (If Applicable)

This is only required if you’re currently making mortgage payments. Make sure it’s the most recent statement and includes the items listed in the worksheet. Checkmark each one as you find it, then checkmark Your Current Mortgage Statement once finished.

Once you’ve gathered all the documents above, submit them either to the secure upload link in your Conditional Pre-Approval email or bring them to any Texas Bay Credit Union branch.

Final Approval & Closing

Once you submit your documents, our team takes over the heavy lifting:

- Document Review: We verify your income and insurance details.

- The Professional Appraisal: We’ll schedule an appraisal to confirm your home’s market value.

- The Texas "Cooling-Off" Period: State law requires a mandatory 12-day waiting period from your initial application before the loan can close.

- Closing & Funding: You’ll sign your final documents at a Texas Bay branch. After a final 3-day right-of-rescission period (standard for primary residences), you will receive your loan.

FAQ: Applying for a Home Equity Loan

How much equity can I borrow against my home in Texas?

In Texas, the total of all loans secured by your home (including your primary mortgage and your new Home Equity Loan or HELOC) cannot exceed 80% of your home’s fair market value. This is a state constitutional requirement designed to protect your home's equity.

What is the difference between a First and Second Lien?

First Lien means your home equity loan will be your only mortgage (either because your home is paid off or you are refinancing your current mortgage into the new loan). A Second Lien is an additional loan taken out while you still have an existing mortgage.

How long does the Texas home equity application process take?

Texas law requires a mandatory 12-day "cooling-off" period from the time you apply/receive notice of your rights until the day the loan can be closed. On average, the whole process—from applying to funding—typically takes 30 to 45 days, depending on how quickly documentation is provided.

Will an appraisal be required for my application?

It depends on your loan amount. For loans of $200,000 or more, a professional appraisal is required to ensure the amount meets the legal 80% limit. While you may use a Harris Central Appraisal District (HCAD) value for your initial estimate, it cannot replace the final professional appraisal for these larger loans. For loans under $200,000, Texas Bay typically only requires an Automated Valuation Model (AVM) estimate.

Can I use a Home Equity Loan for debt consolidation?

Absolutely. Many Texas Bay Credit Union members use their equity to pay off high-interest credit card debt or personal loans, often resulting in a much lower monthly payment and a single, predictable interest rate.

Ready to Get Started?

Applying for a home equity loan or HELOC in Texas doesn’t have to be stressful or tedious. By using our worksheet and gathering your documents in advance, you’ll take the guesswork out of the process and put your goals within reach.

Whether you’re planning a much-needed kitchen remodel or finally consolidating those high-interest credit card balances, you can make it happen with our help.

At Texas Bay Credit Union, we help our neighbors in the Greater Houston community simplify home equity loan requirements in Texas every day. You don’t have to do this alone.

If you have questions about where to start, the 80% rule, or which documents to upload, our team is ready to help. Give us a call or visit a Texas Bay branch near you to get started.