featured

2026-01-09

Personal Finance

published

How to Pay Off Credit Card Debt in 10 Steps

2017-04-24

- Review all your credit card balances and interest rates.

- Refinance and consolidate debts for a simple fixed payment with low interest.

- Use a monthly budget tool to find extra funds for repayment.

- Set up automatic payments to avoid late fees.

- Pay more than the minimum to save thousands in interest.

- Use the Debt Snowball or the Debt Avalanche method to pay your debt down.

Credit card debt impacts millions of Americans, including many in Texas. While credit cards offer convenience and flexibility, carrying a high balance month to month quickly becomes a financial burden.

Carrying expensive interest charges, making the minimum payments, and paying varying amounts on multiple balances make it easy for debt to spiral out of control. At Texas Bay Credit Union, we believe a debt-free life is possible with practical tools, personal discipline, and proper support.

How Does Credit Card Debt Work?

Credit card debt is a type of revolving debt, meaning you can borrow up to a limit and carry a balance month to month with no payoff date. Unlike installment loans with fixed terms and payments, such as a car note, credit cards are flexible but often costly.

The average interest rate on credit card accounts was more than 20.00% APR in 2025, according to the Federal Reserve1. That means carrying a balance can lead to hundreds or thousands of dollars in interest charges over time.

Understanding the cause of your debt is the first step to eliminating it once and for all.

Credit card debt is commonly caused by:

- Emergency expenses (medical bills, car repairs)

- Overspending

- Unemployment or reduced income

- Lack of financial planning or budgeting

Step 1: Assess Your Financial Situation

Lay out your financial information in a way that gives you a view of the complete picture:

- Total income (monthly and annually)

- Fixed expenses (rent, car payment, insurance)

- Variable expenses (groceries, gas, entertainment)

- Total credit card balances

- Interest rates and minimum payments on each card

Gather recent credit card statements and list each credit card with the balance, interest rate, and due date. Once you know where you stand, you can plan to reduce your debt.

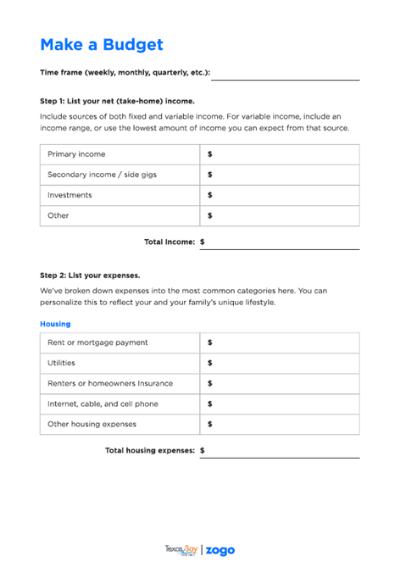

Step 2: Create a Realistic Budget

A monthly budget helps you control spending, identify savings opportunities, and prioritize debt repayment. Use our budget worksheet to get started.

DOWNLOAD YOUR BUDGET WORKSHEET

How to Build Your Budget

- List all monthly income sources in your budget worksheet:

- Salary

- Freelance work

- Benefits

- Any other income streams

- List all monthly expenses (divide annual bills by 12, and semi-annual bills by 6):

- Fixed Expenses

- Annual Expenses (divide these by 12 to see the monthly cost)

- Semi-Annual Expenses (divide these by 6 to see the monthly cost)

- Variable Expenses

- Contributions to Savings

- Find areas to reduce unnecessary spending:

- Dining out

- Unused subscriptions or memberships

- Impulse purchases

- Decide how much you can use to pay off credit card balances each month.

Step 3: Assess Your Income

While spending is a common cause of credit card debt, another is income. Even with a strict budget, you might still struggle with:

- Reliance on credit cards for essential purchases

- Credit card balances that never go down

- Making only the minimum payment each month

- No money left over for an emergency fund

If you’re facing any of the scenarios listed above, even after you’ve cut spending, budgeting may not be the issue. The issue could be cash flow or income.

To confirm this, review your budget sheet and calculate your total monthly expenses, then calculate your total monthly income. Next, subtract the amount of your total monthly expenses from the amount of your total monthly income. The result is your net cash flow.

If your net cash flow is negative, it means you’re earning less than you need. Consider possible ways to bridge the gap, whether it’s exploring additional income sources, reviewing your wages with your employer, or looking into available community resources.

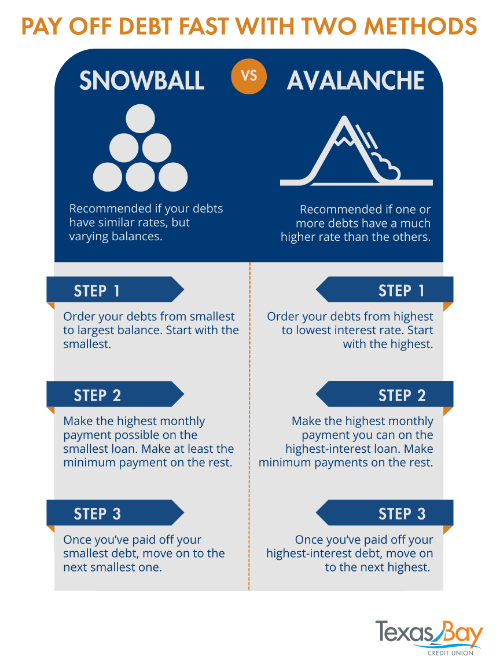

Step 4: Choose a Debt Repayment Strategy

There are two recommended methods for paying off multiple credit cards: the Debt Snowball Method and the Debt Avalanche Method.

.png)

Either method is effective if you stay consistent.

Step 5: Pay More Than the Minimum

Paying the minimum keeps your account in good standing but does little to reduce the principal balance, which can prolong your debt for years.

Consider This Example:

If you owe $5,000 at 20.00% APR, making the minimum monthly payment could take you more than 20 years to pay off the balance and cost you more than $6,000 in interest.

Tips:

- Aim to pay at least double the minimum payment or use any windfall like tax refunds or bonuses to make lump sum payments.

- If your bill date comes before your paycheck, ask your issuer to move your monthly deadline to a date that aligns with your pay cycle so you can pay more each month.

Step 6: Use Balance Transfers Wisely

A balance transfer involves moving high-interest debt from one or more credit cards to another card with a low or zero percent introductory rate. This strategy can save you interest and help you pay off debt faster.

Key Points:

- Many cards offer as low as 0.00% APR for 6 to 18 months

- Balance transfer fees (typically 3 to 5 percent) may apply

- You must have good credit to qualify

Important: Plan to pay off the balance before the promotional period ends, or you may face high deferred interest rates.

Step 7: Explore Debt Consolidation Loans

Debt consolidation is a way to roll multiple high-interest balances into a single loan with a lower, fixed rate—simplifying your monthly bills and reducing total interest. Options include:

- Personal loans, which can reduce your interest rate by half

- Home equity loans or lines of credit, which can reduce your interest rate to a fourth of what it was by using your home as collateral

Texas Bay provides personal and home equity loans tailored to your needs, with fixed interest rates and predictable monthly payments to help you accelerate debt repayment and enjoy financial freedom as quickly as possible.

Step 8: Automate Your Payments

Setting up automatic payments through your online banking system helps you:

- Ensure minimum payments are made on time

- Schedule extra payments if possible

- Avoid late fees

- Maintain a positive payment history

Texas Bay’s mobile and online banking tools make it easy to set up recurring payments.

Step 9: Monitor Your Credit Report and Score

Your credit score influences your ability to qualify for better interest rates and financial products. Credit card debt affects both your score and your report, especially when balances approach the card’s credit limit.

Best Practices:

- Check your credit reports at least annually

- Dispute any errors with the reporting agencies

- Aim to keep your credit utilization ratio below 30 percent

- Track your score monthly with Credit Sense, a free tool available in your Texas Bay digital banking account

Monitoring your credit helps you stay informed and make better financial decisions.

Step 10: Seek Professional Guidance

If managing credit card debt is overwhelming, professional help is available. Nonprofit credit counseling agencies and your local credit union can assist you with personalized financial advice.

Texas Bay Credit Union offers:

- One-on-one FREE Financial Wellness Check Up

- Debt management plans

Our financial professionals will help you navigate your options with confidence and clarity. Schedule an appointment with them today.

FAQ: Paying Off Credit Card Debt

Will paying off my credit card debt improve my credit score immediately?

Your score won’t change right away, but you’ll see an improvement within 30 to 45 days once the credit card issuer reports your new lower balance to the credit bureaus.

Should I close my credit card account once I’ve paid off my debt?

It’s usually better to keep the account open and use it sparingly. Closing a card can shorten your "length of credit history" and reduce your total available credit, which might cause your credit score to drop. If the card has a high annual fee, however, it may be worth closing or switching to one with no fee.

Is it better to save an emergency fund or pay off debt first?

Try to save an emergency fund first. This prevents you from having to use your credit cards again when an unexpected car repair or medical bill arises, which would undo your progress.

Can I negotiate my interest rate directly with my credit card company?

Yes. If you have a history of on-time payments, you can request a lower APR from your issuer. Say that you’re considering a balance transfer to another institution. While not guaranteed, many issuers will offer at least a temporary rate reduction to keep you as a customer.

What is the difference between debt consolidation and debt settlement?

Debt consolidation, such as a personal or home equity loan, combines your debts into a single manageable payment without hurting your credit. Debt settlement involves stopping payments to settle for less than what you owe; this damages your credit score and can stay on your report for seven years.

Does Texas Bay Credit Union offer tools to help me track my debt payoff?

Absolutely. Members can use our Digital Banking platform to monitor spending habits, set up automated transfers, and access free credit monitoring tools to watch their scores grow as their debts shrink.

Take Control of Your Credit Card Debt Today

Credit card debt is daunting, but it’s not permanent. With determination, a realistic plan, and the right resources, you can take control of your finances and eliminate debt for good.

Texas Bay Credit Union is committed to helping our members live financially confident lives. Whether you’re beginning your journey to becoming debt-free or looking for new strategies to manage existing balances, we are here to support you.

Together, we can build a plan tailored to your goals and create a path toward long-term financial wellness.

Contact Texas Bay Credit Union today and speak with a financial specialist.

Sources:

1. Board of Governors of the Federal Reserve System. (2026, January 7). Consumer Credit - G.19. www.federalreserve.gov/releases/g19/current/