featured

2025-12-29

Personal Finance

published

How to Budget, Save, Eliminate Debt & Invest in 2026 | Your New Year Financial Plan

2017-04-24

- Create a budget to track spending, reduce expenses, and increase savings.

- Save enough for three to six months of essential expenses in your emergency fund.

- Refinance and consolidate high-interest debts, like credit cards.

- Use the Snowball or Avalanche method to pay down your debt.

- Contribute to your 401(k), IRA, and low-risk accounts like CDs.

- Contact Texas Bay for personalized financial advice and support.

Is your financial situation holding you back this new year? Are last year’s debt, high expenses, and depleted savings keeping you from reaching your goals? Here’s a three-step plan to help you have your best year yet and set yourself up for even better years ahead.

- Step 1: Create a Budget and Build Your Emergency Savings

- Step 2: Eliminate Debt and Achieve Financial Freedom

- Step 3: Invest and Save for Long-Term Financial Growth

1. How to Create a Budget and Build Your Emergency Savings

- If you didn’t budget during the holidays, it’s time to do so now. Gather your paystubs, statements, and bills from last month.

- List your net income, expenses, debts, and savings contributions.

- Find areas to cut expenses and add to your savings.

- Build your emergency fund with your new savings.

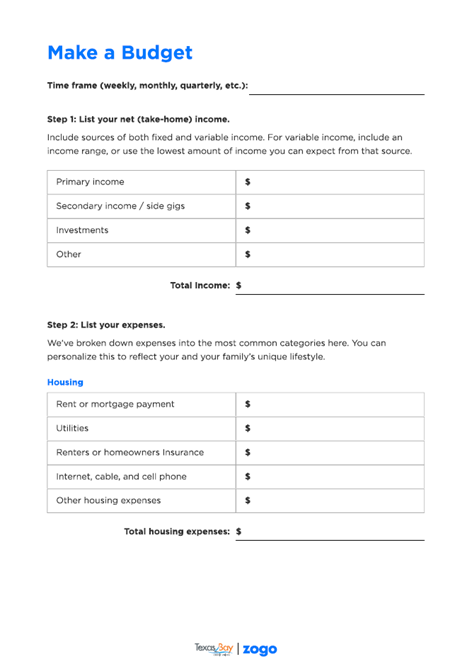

Use our budget worksheet from Zogo to log your income, expenses, and savings goals. You can budget for whichever time frame suits you, but we’re using a monthly budget in our example to match regular monthly bills like rent and utilities.

Download your Budget Worksheet Here:

Follow the worksheet’s instructions while remembering these tips:

- Use previous months’ pay stubs and deposits from your checking account statements to track income.

- Use the average or lowest amount if your income varies.

- Use credit card statements and withdrawals from your checking account statements to track expenses.

- Gather statements from all your bank accounts, credit cards, and bills.

- Divide less frequent expenses to match your budget’s time frame.

- Example: Divide annual HOA dues by 12 to fit a monthly budget.

By the time you finish this worksheet, you will:

- Know where to cut expenses.

- Understand how to approach your emergency savings fund.

What Are the Best Ways to Cut Monthly Expenses and Save Money?

Quick wins to cut expenses include:

- Canceling unused memberships or subscriptions

- Limiting frequent delivery app orders

- Managing impulse purchases

- Opting to cook at home rather than dine out

- Eliminating any habitual purchases that you can live without

However, you don’t have to deprive yourself. Since the changes are meant to be long-term, start with small, manageable cutbacks today and revisit them at least once a month to adjust or add to them.

The money you’ll add back to your budget because of the cutbacks, is your opportunity to put your new savings where they belong.How Do I Build an Emergency Savings Fund for Financial Security?

If you don’t have a savings account for your emergency fund, you should open one right away. Your emergency fund is your financial safety net. It helps you cover unexpected costs, such as car repairs or medical bills, without going into debt.

Your emergency fund account should be:

- Accessible: You need easy, quick access for withdrawals or transfers.

- Safe: Fraud prevention measures like multi-factor authentication and insurance from NCUA or FDIC are a must.

- Separate: This account should not be connected to the daily spending in your checking account.

Once you’ve established your emergency fund, plan to fill it:

Tip: If you have sufficient emergency funds but are concerned about how much you spent over the holidays, consider a Christmas Club savings account to save little by little throughout the year instead of racking up credit card bills or taking out a personal loan. You can open a Christmas Club account at the beginning of the year and contribute as much or as little as you want each month with no withdrawals until November for a stress-free holiday.

Learn about Christmas Club accounts.

Once you have enough in your emergency fund, it’s time to tackle your debt.

2. How to Eliminate Debt and Achieve Financial Freedom

- Frequently review your debt.

- Refinance and consolidate high-interest debt.

- Pay off your debt using the snowball or avalanche method.

- Stick to your budget.

Make a list of your debts and include the following:

- Total amount owed

- Minimum monthly payments

- Due dates

- Interest rate (APR)

If you have a high interest rate on at least one large debt or several smaller ones, your next step should be to lower your interest rate and simplify your monthly payments.

How Do I Refinance High-Interest Debt and Save Money?

If you carry a high credit card debt, the interest rate, or Annual Percentage Rate (APR), on it could be among your biggest financial obstacles:

- High APR: Ranging from 15.00% to over 25.00% APR, interest takes a big chunk of each payment, leaving you on the hook for much more than you borrowed.

- Impacted credit score: The longer it takes to pay off a large debt, the bigger a hit your credit score takes, making it harder for you to qualify for loans in the long run.

- Less financial freedom: The more you pay each month in interest, the less you have for savings, essential expenses, and emergencies.

Your best option would be to refinance that debt with a credit union or bank you trust:

- Personal loans: Get an APR as low as 10.49%. Explore available personal loan options.

- Home equity loans: By using your home as collateral you can lower your APR to a fourth of what it is now. Learn about home equity loans.

- Rate-and-term refinancing: . Your principal will stay the same, but with a new lender, you’ll have a lower rate and a smaller monthly payment. Learn how low your rate could be by making the switch.

Refinancing and consolidating high-interest debt could be the biggest favor you do for yourself this year:

- Lower interest costs: More of each payment goes towards the principal, helping you pay off the debt faster and save money in the process.

- Improved credit health: Consolidating multiple credit card debts into one structured loan will help you reduce your credit utilization and make payments on time, improving your credit score and opening more opportunities for you in the future.

- Financial freedom: With less debt, lower interest rates, and better credit, you’ll have more financial independence than you had last year.

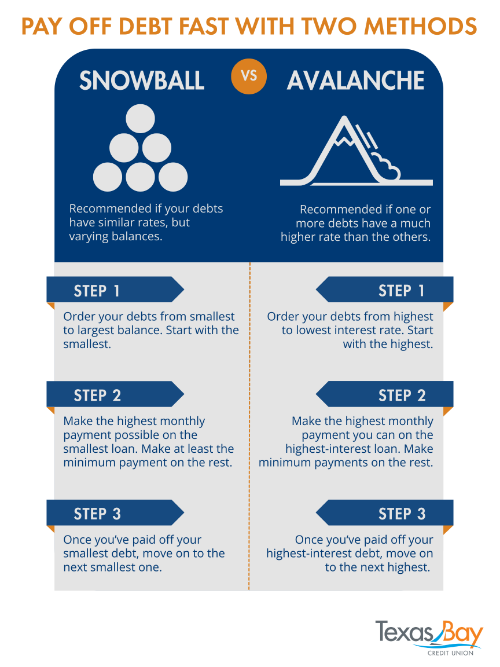

How Do I Pay Off Debts Faster with the Snowball and Avalanche Methods?

Decide how much you want to save each month, but keep in mind that paying off your debt aggressively will help you save more in the long run.

If you have multiple loans of varying amounts, there are two methods to try:

- Snowball Method: Pay off your smallest loan and work your way up from there.

- Avalanche Method: Pay your highest-interest loan first, then work your way down.

.png)

Important tips to remember when paying off debts:

- Pay your debts first—as soon as you get your paycheck. Use autopay if possible.

- Stick to your budget—a missed payment will hurt your credit score.

- Keep going—no matter how long it takes, you’re closer to your goal each month.

Once you’ve managed to pay off your debt, you will have achieved enough financial freedom to take your money to the next level.

3. How to Invest and Save for Long-Term Financial Growth

- Consistently add to your emergency fund.

- Maximize contributions to your 401(k), IRA, or both.

- Practice saving for major goals or milestones.

Whether you dream of retirement or have big plans, it’s never too early to start saving and investing with the right resources. Focus on building your long-term financial future.

Should I Keep Contributing to My Emergency Fund?

Once you meet your emergency fund goal, use your best judgment when deciding how much more to add to it each month. Think about common surprise bills and the likelihood you experience any of them:

- Car repairs

- Home repairs

- Injury or Illness

- Last-minute travel

- Pet emergencies

- Forgotten Subscriptions or Automatic Payments

With that in mind, update how much you’re contributing to your emergency fund.

Remember, these funds should be easily accessible for quick withdrawals and transfers. However, that’s not true for the rest of the money you want to save and invest.

How to Contribute to Your Retirement Funds: 401(k) and IRA

If your employer offers a 401(k) plan, try to contribute enough to get the full employer match, if offered. Any less, and you’re leaving money on the table.

If your employer doesn’t have a 401(k), or you’ve met your employer match and want to explore an additional retirement account, an Individual Retirement Account (IRA) should be the next account you open.

Choose either a Traditional or Roth IRA based on the tax benefits offered:

- Traditional IRA: You won’t pay taxes on your contributions, but you will pay taxes on your withdrawals in retirement.

- Roth IRA: You pay taxes on the money you contribute now, but will withdraw without paying taxes in retirement.

Starting in 2026, you’ll be able to deposit a maximum of $7,500 per year in an IRA, or $8,600 if you’re 50 or older. If you think you’ll meet that limit and want other ways to save and grow your money, you’ve still got plenty of options.

Want to save for your child’s education?

Learn how a Coverdell Education Savings Account helps relieve the burden of tuition costs.

Want a low-risk way to raise money for an upcoming life event or needed upgrade? Consider a certificate of deposit (CD).

How to Grow Your Savings Safely with a CD

If you’re saving for a specific goal, a CD is a great way to grow the money you’ve already set aside for things, including:

- Wedding

- Home down payment

- Car purchase

- Remodeling

- Financial gift for a loved one

- Any upcoming life event, landmark purchase, life upgrade, or investment

The best part: it’s one of the safest ways to grow your savings because it has a set Annual Percentage Yield (APY) that isn’t impacted by the ups and downs of the stock market.

Learn what CD options can help grow your money with little to no risk.

FAQ: Financial Planning and Saving

How much should I save for an emergency fund?

The general rule is to save between three and six months of living expenses for your emergency fund. How much you save can vary based on factors like your job stability, the number of dependents you have, and your personal financial situation.

What are some common mistakes people make when budgeting?

Common mistakes and their consequences when budgeting include:

- Not tracking expenses, which leads to missed opportunities for savings.

- Overestimating income, especially bonuses, which creates budget gaps.

- Underestimating discretionary spending, which makes small purchases add up.

- Not adjusting for changes like unexpected costs, which could impact savings.

What’s the difference between a savings account and an emergency fund?

An emergency fund is a reserve of money set aside for unexpected expenses, such as medical bills or car repairs. A savings account could be used for anything, whether it’s a vacation or a down payment. Keep these funds separate, if possible.

Should I pay off debt or invest first?

It’s a good idea to pay off high-interest debt like credit card debt first. The sooner you do, the more you can earn and save without being outweighed by interest payments when you start investing.

How do I know if refinancing my debt is the right choice for me?

Refinancing may be a good option if:

- You have high-interest debt, like credit card balances.

- You’re eligible for a lower interest rate than the one on your current loan.

- You have multiple loans and want to consolidate them into one monthly payment.

Refinancing may not be ideal if it increases your loan term or if the fees aren’t worth the savings on the interest.

Can I start saving for retirement even if I’m on a tight budget?

Yes, you can! Consistency is the most important thing when contributing to your 401(k) or IRA. Saving however much your budget allows per month is far better than nothing.

Achieve Your Financial Goals with the Right Partner

We understand that everyone has their own financial situation, challenges, and journeys. No matter which step you’re on in this plan or how long it might take you to reach your goals, our goal is for you to be closer to financial independence by this time next year.

Not sure where to begin? We’re here to help you every step of the way. Whether you want to consolidate and eliminate high-interest debt, improve your credit score, or build your savings, a Texas Bay team member can help you make it happen.

Schedule a financial wellness check to review your finances, discuss your goals and challenges, and create a plan to achieve financial freedom.