featured

2026-01-23

Personal Finance

published

How to Overcome Holiday Spending Regret | Texas Bay Credit Union

2017-04-24

- Holiday spending regret is common and temporary.

- Reviewing finances after the holidays helps restore control.

- Small, short-term adjustments can reduce stress and rebuild stability.

- Planning ahead can prevent future holiday overspending.

Understanding Holiday Spending Regret

Holiday spending regret, or post-holiday financial remorse, is common after overspending during the holidays. Small purchases and last-minute expenses add up quickly, leaving strained savings accounts and high credit card balances in January.

In fact, 37% of Americans accumulated holiday debt this past holiday season, according to a recent survey by LendingTree.

You might feel stressed and regretful about your finances after the holidays, but your financial situation isn’t permanent. We can show you how to quickly recover from holiday spending and start the new year confidently.

Assess the Financial Impact of Holiday Spending

Understand how the holidays affected you by reviewing the following.

1. Bank and Credit Card Statements

Identifying your holiday spending habits will help you avoid them next holiday season. Pull your statements and sort expenses into groups like gifts, dining, and travel.

2. Credit Card or Loan Balances

List all balances, interest rates, and minimum payment requirements. This will help you create a plan for your debt repayment or consider a debt consolidation loan for lower interest rates.

3. Emergency Fund

Figure out how much emergency savings you used and if you’re prepared for surprise expenses. Knowing what’s missing from your safety net will help you restore it and your financial security.

4. Monthly Cash Flow

Your available income after expenses determines how soon you can financially recover. Compare your total monthly income against your regular bills (rent, utilities, groceries). This will help you set your budget and find areas to make temporary cuts for a faster recovery.

These assessments will help you build a recovery plan and improve your finances.

Create a Post-Holiday Recovery Plan

Develop a realistic recovery plan to get back on track.

- Set Short-Term Financial Goals

- Build a Monthly Budget

- Pay Off High-Interest Debt

- Reestablish Your Emergency Fund

- Adjust Spending Habits

1. Set Short-Term Financial Goals

Begin with goals that address immediate financial needs following the holidays:

- Paying off high-interest credit card debt

- Rebuilding your emergency fund

- Reducing non-essential spending for the next few months

Celebrate small victories to stay committed throughout the process.

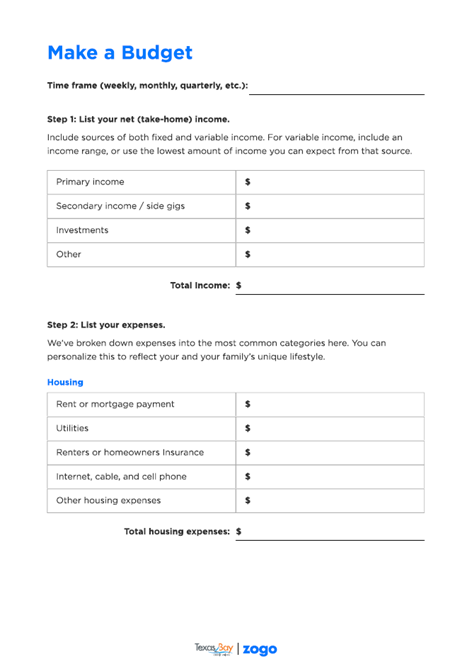

2. Build a Monthly Budget

A monthly budget is vital for staying on top of expenses and saving money.

Download our budget worksheet to get started.

Be sure to include:

- Fixed expenses (utilities and insurance)

- Variable expenses (groceries)

- Debt repayments

- Savings contributions

Focus on paying down debt and rebuilding your savings, even if in small amounts.

Budget for the whole year with free resources and advice from Texas Bay.

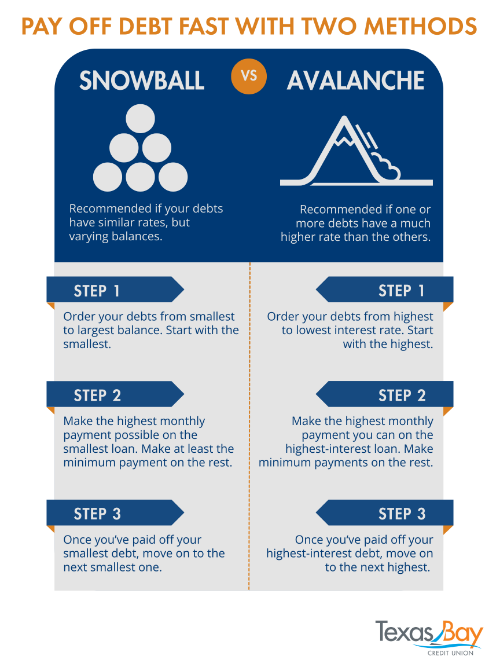

3. Pay Off High-Interest Debt

If you used credit cards during the holidays, prioritize paying off the ones with the highest interest rates. High-interest debt can quickly accumulate and limit your financial progress.

You can clear high-interest debt fast with a couple of simple, proven strategies.

.png)

If you have multiple balances, consolidating debt makes repayment simpler and less stressful:

- Consolidation: Turn multiple debts into a single monthly payment

- Low Interest Rates: Reduce how much you pay in interest when you refinance

- Fixed Terms: Put an end date on your debt and count the days until it’s paid off

Home equity and personal loans are among the best options for refinancing, consolidating, and eliminating credit card debt.

Use our debt consolidation calculator to find out if this is the right solution for you.

4. Reestablish Your Emergency Fund

If your emergency fund was used during the holidays, begin rebuilding it gradually. Setting aside a small, consistent amount each month will restore your safety net.

High-yield savings accounts can make saving easier and more rewarding.

5. Adjust Spending Habits

Recovering financially after the holidays often requires short-term changes to your spending:

- Cook meals at home instead of dining out

- Pause unnecessary subscriptions or memberships

- Limit impulse purchases with a 24-hour rule before buying non-essentials

- Use cash or debit cards to avoid adding to existing credit card balances

These small changes will add up to savings you can use for your debts or emergency fund.

Rebuild Financial Confidence with Tools and Resources

Financial setbacks are temporary, but the habits you build in response can lead to lasting success. Rebuilding confidence in your financial decision-making is an important part of the recovery process.

Take advantage of financial education resources available through your credit union. Texas Bay provides budgeting tools, educational workshops, and personalized financial guidance for members. These resources can empower you to make informed decisions and stay on track.

Get ahead this year with our free education resources.

Plan Ahead for the Next Holiday Season

The best way to avoid future holiday spending regret is to begin planning early. A proactive approach allows you to spread out expenses and avoid last-minute financial strain.

Create a Holiday Budget

Determine how much you want to spend on gifts, travel, and other holiday activities.

Use our holiday budgeting guide to help you set a budget and stay on track.

Saving for the holidays earlier in the year will add flexibility to your budget, too.

Tip: A Christmas Club account lets you contribute a small amount from each paycheck throughout the year with no withdrawals until November. Open your account, set up automatic transfers each month, and watch your holiday fund grow. Explore Christmas Club accounts with Texas Bay.

Shop Strategically Throughout the Year

By shopping during sales and planning ahead, you can avoid paying premium prices in November and December. Keep a list of intended recipients, gifts, and decoration ideas to guide your purchases and stay within budget.

Post-holiday shopping can save you a bundle by shopping during off-peak seasons.

Limit Credit Card Usage

Use cash or debit for holiday purchases whenever possible. If you use credit, ensure it aligns with your monthly budget and repayment plan.

By taking these steps, you can enjoy the next holiday season without stress or regret.

FAQ: Holiday Spending Regret

How long does it take to recover from holiday overspending?

Recovery time can vary, but most people see improvement within a few months by adjusting spending, paying off credit card debt, and gradually rebuilding savings.

How can I avoid overspending during the next holiday season?

Plan early, set spending limits, and save gradually throughout the year to reduce financial stress and prevent last-minute expenses.

Should I focus on saving or paying down debt after the holidays?

Your top three priorities should be your debts, emergency savings, and your essential expenses. Address those three things before you focus on increasing any other kinds of savings.

What if holiday spending affected my emergency fund?

If you used emergency savings, don’t put off replenishing—even if you have debts. Another surprise expense can put you further into debt if you don’t have the funds to cover it.

A Fresh Start with Texas Bay Credit Union

The first weeks after the holidays are an opportunity to get your finances back on track. By understanding your spending and making minor adjustments, you can turn post-holiday regret into progress towards financial freedom.

Want to give yourself the best possible start while you bounce back from the holidays? Schedule a free financial wellness check with an expert at Texas Bay Credit Union and create a personalized plan to help you make holiday spending a cinch.